India’s Data Center (Part 3/4): Technological Transformation & Economy

Industry Expert & Contributor

16 Feb 2026

India's data center sector is undergoing a fundamental technological transformation driven by AI workloads, sustainability imperatives, and resource constraints. This shift is redefining competitive advantage from traditional metrics like physical capacity to advanced engineering capabilities in cooling, power management, and resource efficiency.

The AI-Driven Infrastructure Revolution

From Air to Liquid: The Cooling Paradigm Shift

The proliferation of AI and high-performance computing workloads is rendering traditional data center infrastructure obsolete. Rack densities are increasing from 5-10 kW for conventional enterprise applications to 50-120 kW for AI training and inference workloads. This tenfold increase fundamentally exceeds the thermal management capacity of air-cooling systems.

Air's low heat capacity creates a hard physical limit. At rack densities above 30-40 kW, air-cooling systems require excessive airflow volumes, creating acoustic issues, energy inefficiency, and space constraints. Liquid-based cooling, including direct-to-chip cold plates and immersion cooling, has transitioned from experimental to operational necessity.

- Performance Improvements: Empirical research and production deployments demonstrate that liquid cooling delivers approximately 25-35% improvements in energy efficiency compared to conventional air systems. More critically, liquid cooling enables compute densities that would be physically impossible with air, supporting over 100 kW per rack in operational environments.

- Economic Implications: While liquid cooling systems carry higher upfront capital costs (approximately 15-20% premium), operational savings through reduced energy consumption typically achieve payback within 3-4 years. For AI-optimised facilities with 10-15 year operational horizons, this represents compelling unit economics.

- Market Adoption: Leading Indian operators are deploying liquid cooling in new AI-focused facilities. Production environments are achieving Power Usage Effectiveness (PUE) values near 1.3, significantly outperforming the global data center average of 1.5-1.8. A PUE of 1.3 means only 0.3 kW of auxiliary power supports each 1 kW of IT load, directly impacting operational profitability.

- Strategic Consideration: Facilities not designed for liquid cooling face significant retrofit challenges. Existing buildings often lack adequate floor loading, drainage systems, and leak detection infrastructure required for liquid cooling deployment. This creates a structural advantage for greenfield developments and poses obsolescence risk for legacy assets.

Power Infrastructure: From Operational Issue to Strategic Differentiator

The Grid Reliability Challenge

Although data centers currently consume less than 0.5% of India's total electricity, this share masks the sector's true infrastructure impact. Mission-critical digital infrastructure requires reliability standards exceeding 99.999% uptime, “five nines”, translating to less than 5.26 minutes of downtime annually.

Many regional grids do not consistently meet this standard, forcing operators to maintain expensive redundant backup systems. Traditional diesel generators introduce both economic costs (fuel, maintenance) and environmental liabilities (emissions, regulatory scrutiny). The transition to battery energy storage systems (BESS) and hybrid renewable solutions offers alternatives but requires substantial upfront investment.

The Coming Power Crunch

Projected growth trajectories reveal power as the binding constraint on sector expansion:

- 2024 baseline: <0.5% of national electricity generation

- 2026 projection: ~2% of national electricity demand (~1,825 MW)

- 2030 projection: ~8% of national electricity demand (~17 GW IT capacity)

This exponential growth, from marginal to material national electricity consumption within six years, transforms power sourcing from operational consideration to strategic infrastructure question. Localized grid stress in high-density metros (Mumbai, Chennai, Hyderabad) is already constraining new capacity additions.

Regional Variability Creates Winners and Losers

Grid reliability varies dramatically across states, creating location-specific execution risk. Coastal metros with mature industrial infrastructure and multiple grid interconnections demonstrate higher "five nines" capability. Inland and Tier-2 regions face execution challenges despite lower land costs and state incentives.

Site Selection Implications: Power reliability is increasingly trumping traditional location factors. Operators are prioritizing sites with:

- Proven grid stability and multiple redundant connections

- Proximity to generation sources (reducing transmission losses and bottlenecks)

- Access to dedicated industrial power feeders

- State policies supporting captive generation and energy storage

Capital Intensity and Tariff Sensitivity

Development costs of INR 60-70 crore (USD 7.2-8.4 million) per megawatt include substantial power infrastructure investments: substations, transformers, switchgear, backup systems, and grid connectivity. These costs are rising due to equipment inflation and more stringent technical specifications for AI workloads.

Inter-state electricity tariff differentials materially influence long-term economics. Variations of 20-30% in base power costs, combined with different renewable energy access and banking provisions, create significant operational expense differences over 10-15 year facility lifecycles.

Strategic Response: Leading operators are pursuing vertical integration strategies, developing captive renewable generation, long-term PPAs, and energy storage to hedge tariff volatility and ensure supply reliability. This shifts competitive advantage toward firms with energy expertise and balance sheet capacity for infrastructure investment.

Water: The Constraint Nobody Saw Coming

Thermal Management Meets Water Scarcity

Evaporative cooling systems—standard in many Indian data centers due to climate conditions—require up to 25 million liters of water per megawatt annually. In water-stressed metros like Chennai and Mumbai, this consumption level creates regulatory, operational, and reputational risk.

Water scarcity is being exacerbated by climate variability, urban population growth, and competing industrial demands. Data centers are increasingly competing with municipal water supply, agriculture, and other industries for finite resources. This positions water availability as a constraint potentially equal to power in determining site viability.

Regulatory Tightening and WUE Benchmarks

Mandatory water impact assessments are now required for data center projects in Chennai and Mumbai, with other metros expected to follow. The Indian Green Building Council (IGBC) has established Water Usage Effectiveness (WUE) benchmarks below 2.2 liters per kWh as targets for certification.

Leading operators are implementing circular water management systems:

- Rainwater harvesting to supplement municipal supply

- Treated sewage water (TSW) for cooling systems

- Closed-loop cooling to minimise evaporative losses

- On-site water recycling facilities

Case Example: CtrlS Datacenters has recycled approximately 10 million liters of water, demonstrating feasibility of transitioning from linear to circular water use. This operational track record is becoming a competitive differentiator in site approvals and client procurement decisions.

Water as Resilience Metric

Facilities with low WUE (<2.0 liters per kWh) and integrated recycling systems demonstrate higher long-term operational resilience, particularly in climate-variable regions. As drought frequency increases and regulatory scrutiny intensifies, water efficiency is transitioning from sustainability credential to operational necessity.

Investment Implication: Water infrastructure, recycling systems, rainwater harvesting, closed-loop cooling, represents 5-8% of total facility capex but significantly reduces regulatory risk and operational vulnerability. Investors should evaluate water strategy with the same rigor as power strategy in due diligence.

Sustainability: From CSR to Competitive Advantage

The Economic Case for Green Infrastructure

The sustainability transition in India's data center sector is now driven by operational economics rather than regulatory compliance or corporate values. Cooling systems account for approximately 40% of total data center energy consumption, making thermal efficiency directly translatable to bottom-line profitability.

Advanced cooling and energy management strategies deliver measurable financial returns:

- 25-35% energy efficiency improvements from liquid cooling vs. air cooling

- PUE reduction from 1.7-1.8 to 1.3 cuts operational power costs by ~25%

- Long-term renewable PPAs provide 10-20 year price stability, hedging grid tariff volatility

Renewable Energy Integration: From Target to Operational Reality

Major operators are committing to 100% renewable energy by 2030, but execution models vary significantly:

- On-site Solar Generation: Rooftop and campus solar installations provide 10-15% of facility power requirements, reducing grid dependency and demonstrating sustainability credentials. However, intermittency and land constraints limit scalability.

- Long-term PPAs: 15-25 year renewable power purchase agreements with wind and solar developers provide price certainty and large-scale renewable access. These contracts are increasingly structured as "round-the-clock" (RTC) products combining solar, wind, and battery storage to address intermittency.

- Grid-scale Partnerships: Operators are partnering with utilities and renewable developers on dedicated generation capacity. Examples include NTT's renewable partnerships and Google's renewable energy initiatives supporting Indian operations.

- Battery Energy Storage Systems (BESS): Advanced storage technologies enable operators to store renewable energy during generation peaks and dispatch during demand peaks or generation troughs. BESS systems also provide backup power, potentially replacing diesel generators.

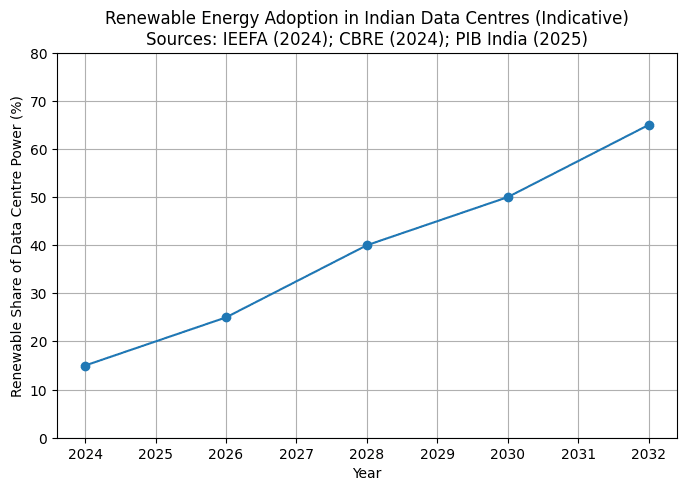

Current and Projected Renewable Penetration

Sector-wide renewable energy penetration is expected to increase from approximately 10-15% currently to around 30% by 2030, supported by fiscal incentives in the Draft National Data Centre Policy (2025). Leading operators are targeting more aggressive timelines:

- 2024 baseline: 10-15% renewable penetration

- 2026 projection: 15-20% renewable penetration

- 2030 target: 30%+ renewable penetration (policy-supported trajectory)

- Leading operators: 50-70% renewable targets by 2028, 100% by 2030

Policy Alignment Accelerates Transition

The Draft National Data Centre Policy (2025) proposes fiscal incentives for green-certified facilities, including:

- Tax benefits for renewable-powered data centers

- Accelerated depreciation for energy-efficient equipment

- Priority grid connectivity for facilities meeting sustainability benchmarks

- Expedited environmental approvals for water-efficient designs

This policy alignment integrates sustainability directly into project economics, transforming green infrastructure from cost center to value creator. States like Gujarat and Rajasthan are positioning themselves as renewable-driven data center destinations, leveraging abundant solar resources and lower land costs.

ESG as Procurement Requirement

Hyperscale cloud providers and multinational enterprises increasingly mandate renewable energy and carbon-efficiency thresholds in colocation procurement. Sustainability certifications, LEED, IGBC, Energy Star, are shifting from differentiators to baseline requirements.

Market Impact: Operators unable to demonstrate credible renewable energy strategies and low PUE/WUE performance face exclusion from hyperscale and enterprise RFPs. This creates bifurcation between sustainability-leaders capturing premium clients and laggards competing on price in commoditized segments.

The Economics of Long-term Renewable PPAs

Long-term renewable PPAs (15-25 years) provide three distinct advantages:

- Price Stability: Fixed or predictable pricing insulates operators from grid tariff volatility and fuel cost fluctuations

- Cost Competitiveness: Renewable energy costs have declined 60-70% over the past decade, making wind/solar PPAs cost-competitive with or cheaper than grid power in many regions

- Client Requirements: Hyperscale and enterprise clients increasingly require renewable energy commitments as procurement criteria

Strategic Implication: Renewable energy strategy has transitioned from sustainability initiative to core business strategy. Operators with long-term renewable PPAs demonstrate lower operational risk, more predictable cash flows, and stronger competitive positioning.

Geographic Redistribution: Tier-2 Cities Emerge

The Hub-and-Spoke Architecture

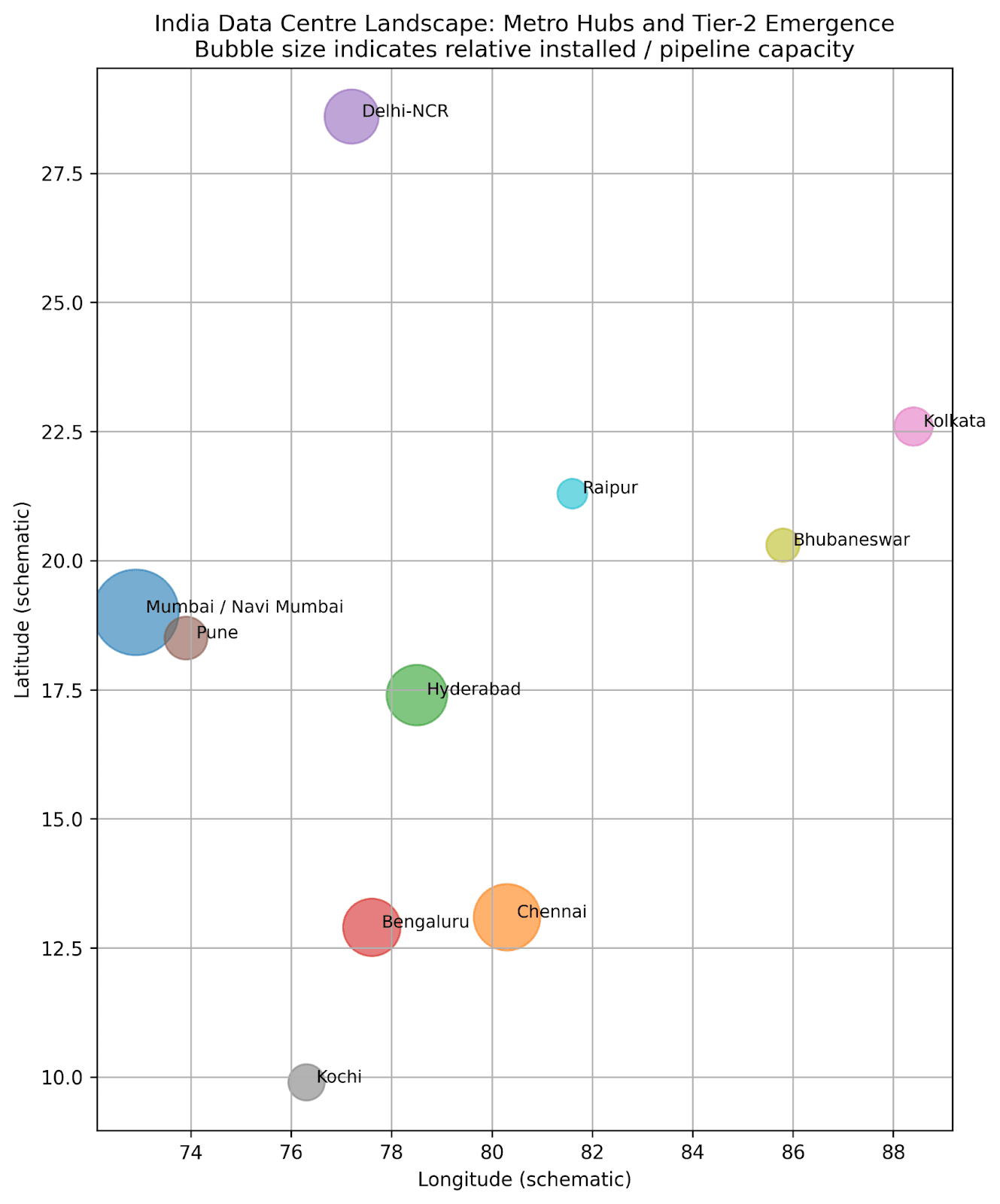

India's data center capacity is undergoing geographic redistribution. While Tier-1 metros (Mumbai, Chennai, Hyderabad, Bengaluru) retain advantages in subsea cable connectivity, fiber density, and enterprise proximity, Tier-2 cities are emerging as strategic locations for specific workloads.

Tier-2 Advantages:

- Land Costs: 40-60% lower than Tier-1 metros

- Approval Speed: Faster permitting in less congested regulatory environments

- State Incentives: Aggressive incentive packages (capital subsidies, power tariff support, tax benefits)

- Power Availability: Less grid congestion, better access to dedicated industrial feeders

- Water Access: Lower competition for water resources

Tier-2 Use Cases:

- Edge Computing: Latency-sensitive applications for regional populations (gaming, telemedicine, real-time analytics)

- AI Inference: Post-training inference workloads with less demanding connectivity requirements

- Disaster Recovery: Geographic diversification for business continuity

- Content Caching: CDN and streaming infrastructure serving regional demand

Emerging Tier-2 Hubs: Pune, Jaipur, Kochi, Bhubaneswar, Noida, Greater Noida, and Raipur are attracting investment. RackBank's 80 MW AI-focused facility in Raipur exemplifies this trend, leveraging central India location, renewable energy access, and state incentives.

Infrastructure Gap Reality Check

Tier-2 advantages come with execution trade-offs. Power redundancy, fiber network depth, and water recycling infrastructure are still evolving. This creates a risk-return trade-off: lower costs and faster approvals vs. infrastructure maturity and operational complexity.

Strategic Approach: Leading operators are pursuing phased Tier-2 deployment, starting with edge-first use cases and expanding to more demanding workloads as infrastructure matures. This de-risks execution while capturing cost advantages.

Market Structure Evolution: From Oligopoly to Differentiated Competition

The Changing Competitive Landscape

India's data center ecosystem is transitioning from concentrated oligopoly to differentiated competition. Early market concentration among 3-4 dominant players is giving way to a more diverse competitive landscape spanning hyperscale self-builds, global colocation providers, domestic operators and specialised AI infrastructure players.

Market Segmentation:

- Hyperscale Self-Builds: AWS, Microsoft Azure, and Google Cloud are increasingly developing custom-built facilities for proprietary workloads, particularly AI training and large-scale cloud services. This vertical integration reduces reliance on third-party colocation and establishes performance benchmarks that pressure colocation providers.

- Global Colocation Leaders: STT GDC, NTT, Equinix leverage global operating standards, international capital access, and established enterprise relationships. These operators target multinational clients requiring consistent global infrastructure and proven operational track records.

- Domestic Champions: CtrlS, Yotta, Web Werks leverage local market knowledge, government relationships, and integrated development capabilities. These operators demonstrate agility in navigating India's complex regulatory environment and establishing regional presences.

- Conglomerate Entrants: Adani, Reliance are deploying integrated models combining data centers with power generation, real estate, and telecommunications. This vertical integration creates competitive advantages in power sourcing, site development, and client bundling but requires massive capital commitments.

- AI Infrastructure Specialists: RackBank and emerging players are developing GPU-optimised facilities with liquid cooling, high-density power, and low-latency networking specifically for AI workloads. This specialisation targets the fastest-growing, highest-margin market segment.

Technology as Competitive Differentiator

Equipment and cooling markets remain moderately fragmented, with global suppliers (Schneider Electric, Vertiv, Carrier) establishing performance standards and domestic manufacturers competing on cost and localization. Operators with early-mover advantage in liquid cooling, advanced DCIM systems, and integrated renewable energy are capturing disproportionate market share.

Innovation-Driven Differentiation: The market is shifting from commodity colocation to technology-enabled platforms. Operators offering:

- Liquid cooling supporting >50 kW racks

- PUE <1.3 and WUE <2.0 liters/kWh

- 100% renewable energy with RTC supply

- AI-driven facility management and predictive maintenance

- Integrated edge-to-cloud architectures

...are capturing premium pricing and preferred hyperscale partnerships.

The Race for AI Infrastructure

AI workload proliferation is creating a sub-market within the broader data center sector. GPU-dense facilities with specialized cooling, power, and networking requirements command premium pricing but face higher execution complexity and capital intensity.

- Market Opportunity: Industry consensus suggests AI-related workloads could comprise 50% of total data center capacity within the next decade. This represents massive addressable market expansion but requires operators to completely reimagine facility design, operations, and business models.

- Entry Barriers Rising: The technical requirements for AI-optimised infrastructure, liquid cooling expertise, high-voltage power distribution, GPU cluster networking, advanced facility management, create natural barriers favoring operators with engineering depth and capital resources.

Strategic Imperatives for Technology Leadership

Engineering Excellence as Competitive Moat

Future market leadership will accrue to operators demonstrating:

- Thermal Management Innovation: Liquid cooling deployment expertise, hybrid cooling strategies, and continuous PUE optimization

- Power Resilience: Multi-source power strategies combining grid, renewables, and storage with >99.999% reliability

- Water Circularity: Closed-loop cooling, rainwater harvesting, and WUE <2.0 liters/kWh

- AI-Ready Design: Modular infrastructure supporting rapid capacity scaling and technology evolution

- Operational Intelligence: AI-driven DCIM systems for predictive maintenance, dynamic load optimisation, and real-time efficiency management

Integration as Strategic Advantage

Firms successfully integrating power generation, cooling infrastructure, fiber connectivity, and facility operations achieve:

- Lower Lifecycle Costs: 15-20% operational cost advantages through vertical integration

- Higher Switching Barriers: Bundled services create client stickiness

- Faster Execution: Reduced dependency on third-party vendors accelerates deployment

- Risk Mitigation: Control over critical infrastructure reduces external dependencies

The Adani-Google AdaniConneX model exemplifies this approach, combining data centers, renewable energy and telecommunications under unified ownership.

Technology Determines Market Winners

India's data center transformation is fundamentally a story of technological evolution. Competitive advantage has shifted from traditional infrastructure metrics, square footage, power capacity, geographic presence, to advanced engineering capabilities in cooling, power management, and resource efficiency.

Operators unable to deploy liquid cooling, achieve PUE <1.3, implement circular water management, and secure long-term renewable energy will face margin compression and market share loss. Those demonstrating technology leadership will capture premium hyperscale partnerships, AI infrastructure opportunities, and sustainable competitive advantage.

The next 3-5 years will separate technology leaders from infrastructure laggards. Execution excellence in engineering innovation, sustainability integration and operational optimisation will determine market winners in India's data center transformation.